There is a lot of chatter on CNBC about poor market breadth. I can see why. On Friday most market averages were at new highs so one would expect the Advance-Decline Line to also be at a high. It wasn’t. The well published AD Line based on NYSE data failed to reach a high. I’m not worried, however. In my view this is a case of garbage in-garbage out.

To measure market participation, or market breadth, most analysts look at the number of stocks advancing on the NYSE versus the number of declining stocks. Here’s the problem: Close

to half of the securities traded on the NYSE are closed-end bond funds that are tied to interest rates, ADRs and warrents. With the move higher in interest rates, the bond funds are moving lower. So upon first glance it looked like many stocks are declining. While advancing and declining figures are technically correct, they are misleading because about half of the issues represent “irregular” securities.

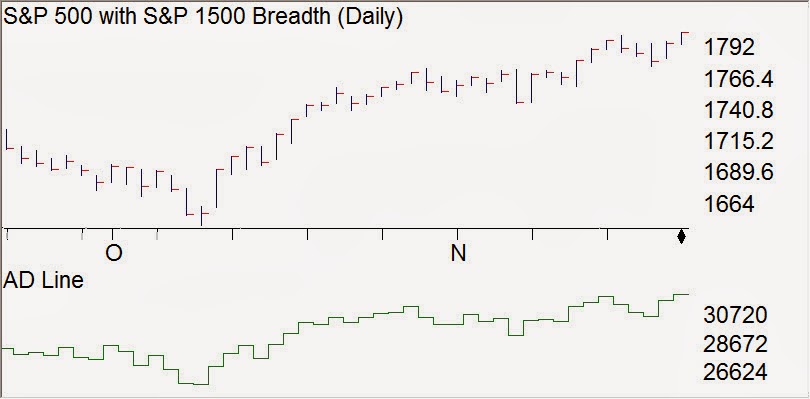

Instead of using the flawed NYSE data, it’s best to run market breadth calculations on a large list of stocks that excludes bond funds. For my analysis, I crunch the numbers on the 1500 stocks in the S&P 1500 index. As the chart shows, the Advance Decline Line reached a new high on Friday. Market breadth is strong.

As interest rates trend higher, we’ll hear even more analysts warning about the market’s poor market breadth. It’s not that these analyst’s calculations are wrong, it’s that the data they use in their calculation is flawed.

As interest rates trend higher, we’ll hear even more analysts warning about the market’s poor market breadth. It’s not that these analyst’s calculations are wrong, it’s that the data they use in their calculation is flawed.

David Vomund is a fee-only Registered Investment Advisor. Information is found at www.ETFportfolios.net. Past performance does not guarantee future results. Consult your financial advisor before purchasing any security.